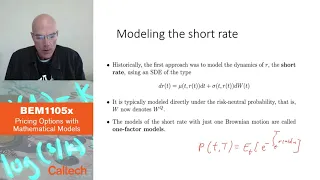

Mathematical finance | Interest rates | Short-rate models

Short-rate model

A short-rate model, in the context of interest rate derivatives, is a mathematical model that describes the future evolution of interest rates by describing the future evolution of the short rate, usually written . (Wikipedia).

.png?width=300)