Summary statistics | Matrices | Covariance and correlation

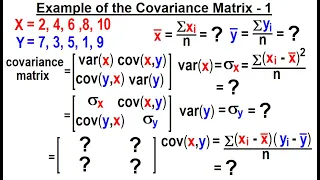

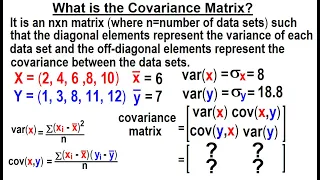

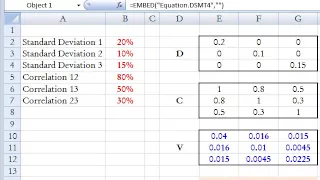

Covariance matrix

In probability theory and statistics, a covariance matrix (also known as auto-covariance matrix, dispersion matrix, variance matrix, or variance–covariance matrix) is a square matrix giving the covariance between each pair of elements of a given random vector. Any covariance matrix is symmetric and positive semi-definite and its main diagonal contains variances (i.e., the covariance of each element with itself). Intuitively, the covariance matrix generalizes the notion of variance to multiple dimensions. As an example, the variation in a collection of random points in two-dimensional space cannot be characterized fully by a single number, nor would the variances in the and directions contain all of the necessary information; a matrix would be necessary to fully characterize the two-dimensional variation. The covariance matrix of a random vector is typically denoted by or . (Wikipedia).