RT6. Representations on Function Spaces

Representation Theory: We note how to transfer a group action of a group G on a set X to a group action on F(X), the functions on X. Because F(X) is a vector space, we obtain a representation of the group, and we can apply previous techniques. In particular, the group acts on itself in

From playlist Representation Theory

In this video, I explain function space and how to change the basis vectors we use to describe function. This lead us to a different understanding of Taylor series, Fourier series and most series. I also explain the Heisenberg uncertainty principle using function space. Additionnal video

From playlist Summer of Math Exposition Youtube Videos

Representation theory: Introduction

This lecture is an introduction to representation theory of finite groups. We define linear and permutation representations, and give some examples for the icosahedral group. We then discuss the problem of writing a representation as a sum of smaller ones, which leads to the concept of irr

From playlist Representation theory

Representation theory: Frobenius groups

We recall the definition of a Frobenius group as a transitive permutation group such that any element fixing two points is the identity. Then we prove Frobenius's theorem that the identity together with the elements fixing no points is a normal subgroup. The proof uses induced representati

From playlist Representation theory

Mike Boyle - Nonnegative matrices : Perron Frobenius theory and related algebra (Part 1)

Lecture I. I’ll give a complete elementary presentation of the essential features of the Perron Frobenius theory of nonnegative matrices for the central case of primitive matrices (the "Perron" part). (The "Frobenius" part, for irreducible matrices, and finally the case for general nonnega

From playlist École d’été 2013 - Théorie des nombres et dynamique

C73 Introducing the theorem of Frobenius

The theorem of Frobenius allows us to calculate a solution around a regular singular point.

From playlist Differential Equations

Cayley-Hamilton Theorem: General Case

Matrix Theory: We state and prove the Cayley-Hamilton Theorem over a general field F. That is, we show each square matrix with entries in F satisfies its characteristic polynomial. We consider the special cases of diagonal and companion matrices before giving the proof.

From playlist Matrix Theory

Mike Boyle - Nonnegative matrices : Perron Frobenius theory and related algebra (Part 4)

Lecture I. I’ll give a complete elementary presentation of the essential features of the Perron Frobenius theory of nonnegative matrices for the central case of primitive matrices (the "Perron" part). (The "Frobenius" part, for irreducible matrices, and finally the case for general nonnega

From playlist École d’été 2013 - Théorie des nombres et dynamique

Cayley-Hamilton Theorem Example 2

Matrix Theory: Let A be the 3x3 matrix A = [1 2 2 / 2 0 1 / 1 3 4] with entries in the field Z/5. We verify the Cayley-Hamilton Theorem for A and compute the inverse of I + A using a geometric power series.

From playlist Matrix Theory

Marie-Claire Quenez: European and american optionsin a non-linear incomplete market with default

HYBRID EVENT Recorded during the meeting "Advances in Stochastic Control and Optimal Stopping with Applications in Economics and Finance" the September 12, 2022 by the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video a

From playlist Probability and Statistics

Fin Math L5-3: Towards Black-Scholes-Merton

Welcome to the last part of Lesson 5. In this video we cover some last relevant topics to finally deal with the Black-Scholes-Merton theorem, which will be the starting point of all our pricing exercises. Here you can download the new chapter of the lecture notes: https://www.dropbox.com/s

From playlist Financial Mathematics

Paolo Guasoni, Lesson I - 18 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

Fin Math L6-1: The Black-Scholes-Merton theorem

Welcome to Lesson 6 of Financial Mathematics. This is the lesson of the Black-Scholes-Merton (BSM) theorem. Finally, you might say. But it will also be the lesson of volatility and distortions. A lot of interesting things. In this first video, we focus on the BSM theorem. Topics: 00:00 I

From playlist Financial Mathematics

Fin Math L5-2: A simple exchange rate model

In this second part of Lesson 5, we consider a simple exchange rate model, which allows us to see the Cameron-Martin theorem in action. The model also introduces a particular version of the exponential martingale that will be essential for us later. I ask you to spend some time reasoning a

From playlist Financial Mathematics

Experimentation with Temporal Interference: by Peter W Glynn

PROGRAM: ADVANCES IN APPLIED PROBABILITY ORGANIZERS: Vivek Borkar, Sandeep Juneja, Kavita Ramanan, Devavrat Shah, and Piyush Srivastava DATE & TIME: 05 August 2019 to 17 August 2019 VENUE: Ramanujan Lecture Hall, ICTS Bangalore Applied probability has seen a revolutionary growth in resear

From playlist Advances in Applied Probability 2019

Hans Föllmer: Entropy, energy, and optimal couplings on Wiener space

HYBRID EVENT Recorded during the meeting "Advances in Stochastic Control and Optimal Stopping with Applications in Economics and Finance" the September 12, 2022 by the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video a

From playlist Probability and Statistics

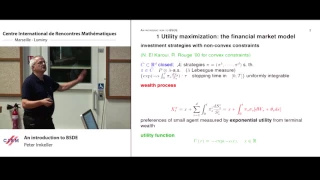

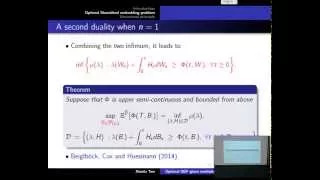

Peter Imkeller: An introduction to BSDE

Abstract: Backward stochastic differential equations have been a very successful and active tool for stochastic finance and insurance for some decades. More generally they serve as a central method in applications of control theory in many areas. We introduce BSDE by looking at a simple ut

From playlist Probability and Statistics

Martin Larsson: Affine Volterra processes and models for rough volatility

Abstract: Motivated by recent advances in rough volatility modeling, we introduce affine Volterra processes, defined as solutions of certain stochastic convolution equations with affine coefficients. Classical affine diffusions constitute a special case, but affine Volterra processes are n

From playlist Probability and Statistics

Xiaolu Tan: On the martingale optimal transport duality in the Skorokhod space

We study a martingale optimal transport problem in the Skorokhod space of cadlag paths, under finitely or infinitely many marginals constraint. To establish a general duality result, we utilize a Wasserstein type topology on the space of measures on the real value space, and the S-topology

From playlist HIM Lectures 2015

Boris Adamczewski: Mahler's method in several variables

Abstract: Any algebraic (resp. linear) relation over the field of rational functions with algebraic coefficients between given analytic functions leads by specialization to algebraic (resp. linear) relations over the field of algebraic numbers between the values of these functions. Number

From playlist Combinatorics