Intermittent Planetary Mechanism

This mechanism produces a reciprocating movement, with the forward always longer than the backward. It uses a planetary mechanism with two inputs, the sun and the ring. The output is the arm. The inputs are provided by an intermittent mechanism, with one gear moving two others, one at a ti

From playlist Planetary Mechanisms

Describes what acceleration is in physics, how to calculate acceleration and how to determine if an object is speeding up, slowing down or moving at a constant velocity based on the direction of it velocity and acceleration vectors You can see a listing of all my videos at my website, http

From playlist Motion Graphs; Position and Velocity vs. Time

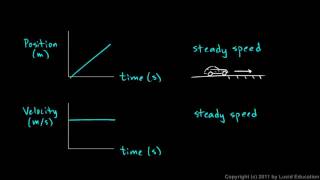

Motion Graphs (3 of 8) Position vs. Time Graph Part 3, Constant Velocity and Acceleration

Describes how to determine the characteristics of an objects motion from its position vs time graph. You can see a listing of all my videos at my website, http://www.stepbystepscience.com Motion graphs are an excellent way to get an understanding of an objects motion over time. The slope

From playlist Motion Graphs; Position and Velocity vs. Time

Physical Science 1.8g - Graphs - Constant Velocity

Position and Velocity graphs for the particular case of constant velocity.

From playlist Physical Science Chapter 1 (Complete chapter)

C68 The physics of damped motion

See how the graphs of damped motion changes with changes in mass, the spring constant, and the initial value constants. The equations tell us which parameters influence the period, frequency and amplitude of oscillation.

From playlist Differential Equations

Stationary Points: Step-by-Step Guide

More resources available at www.misterwootube.com

From playlist Applications of Differentiation

Trend Modeling by Chiranjit Mukhopadhyay

Program Summer Research Program on Dynamics of Complex Systems ORGANIZERS: Amit Apte, Soumitro Banerjee, Pranay Goel, Partha Guha, Neelima Gupte, Govindan Rangarajan and Somdatta Sinha DATE : 15 May 2019 to 12 July 2019 VENUE : Madhava hall for Summer School & Ramanujan hall f

From playlist Summer Research Program On Dynamics Of Complex Systems 2019

Review of Linear Time Invariant Systems

http://AllSignalProcessing.com for more great signal-processing content: ad-free videos, concept/screenshot files, quizzes, MATLAB and data files. Review: systems, linear systems, time invariant systems, impulse response and convolution, linear constant-coefficient difference equations

From playlist Introduction and Background

Introducing Time Series Forecasting in Python: the Random Walk Forecast

Check out Marco Peixeiro's book 📖 Time Series Forecasting in Python | http://mng.bz/95Mr 📖 To save 40% on Marco's book use the DISCOUNT CODE ⭐ watchpeixeiro40 ⭐ Join Marco in this introductory lesson on time series forecasting in Python. Marco explores the random walk model, MA(q) and

From playlist Python

Anne Leucht: Mixing properties of (non-)stationary INGARCH(1,1) processes

CONFERENCE Recording during the thematic meeting : "Adaptive and High-Dimensional Spatio-Temporal Methods for Forecasting " the September 27, 2022 at the Centre International de Rencontres Mathématiques (Marseille, France) Filmmaker: Guillaume Hennenfent Find this video and other talks

From playlist Probability and Statistics

Stilian Stoev: Function valued random fields: tangents, intrinsic stationarity, self-similarity

We study random fields taking values in a separable Hilbert space H. First, we focus on their local structure and establish a counterpart to Falconer's characterization of tangent fields. That is, we show (under general conditions) that the tangent fields to a H-valued process are self-sim

From playlist Probability and Statistics

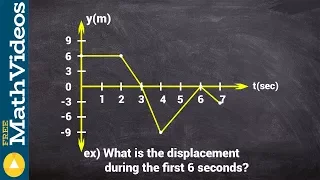

What is the displacement of a particle from a position graph

Keywords 👉 Learn how to solve particle motion problems. Particle motion problems are usually modeled using functions. Now, when the function modeling the position of the particle is given with respect to the time, we find the speed function of the particle by differentiating the function

From playlist Particle Motion Problems

Simple Harmonic Motion (2 of 16): Pendulum, Calculating Period, Frequency, Length and Gravity

In this video I go over five example problems for calculating the period, frequency, length and acceleration due to gravity for a simple pendulum. A pendulum is a mass suspended from a string that is attached to pivot point. There is no friction so that the pendulum can swing freely. When

From playlist Simple Harmonic Motion, Waves and Vibrations

Time Series class: Part 1 - Dr Ioannis Papastathopoulos, University of Edinburgh

Part 2: https://youtu.be/7n0HTtThMe0 Introduction: Moving average, Autoregressive and ARMA models. Parameter estimation, likelihood based inference and forecasting with time series. Advanced: State-space models (hidden Markov models, Kalman filter) and applications. Recurrent neural netw

From playlist Data science classes

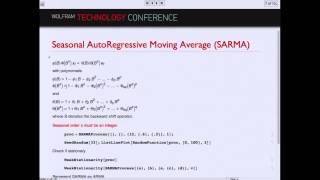

QRM 7-1: TS for RM 2 (seasons, ARMA and more)

Welcome to Quantitative Risk Management (QRM). Lesson 7 is very rich. In part 1, we start from seasonality and how to deal with it (more applied details in QRM 7-3). We then introduce AR, MA and ARMA processes, discussing their basic properties, like causality and invertibility. To suppo

From playlist Quantitative Risk Management

Data Science - Part X - Time Series Forecasting

For downloadable versions of these lectures, please go to the following link: http://www.slideshare.net/DerekKane/presentations https://github.com/DerekKane/YouTube-Tutorials This lecture provides an overview of Time Series forecasting techniques and the process of creating effective for

From playlist Data Science

Welcome to Quantitative Risk Management (QRM). In Lesson 6 we start discussing Time Series (TS) analysis, which we will later combine with EVT. We will answer the following questions: What is a TS? What types of TS can we model? What does stationarity mean? What are the main causes of non

From playlist Quantitative Risk Management

Deep Learning Lecture 7.2 - Slow Manifolds

Learning Slow Manifolds with Markovian methods: Introduction and learning problem.

From playlist Deep Learning Lecture

Gosia Konwerska discusses some of the tools for time series analysis in Mathematica in this presentation from the Wolfram Technology Conference. For more information about Mathematica, please visit: http://www.wolfram.com/mathematica

From playlist Wolfram Technology Conference 2012

Graphing Stationary Points (1 of 3: Using the first derivative)

More resources available at www.misterwootube.com

From playlist Applications of Differentiation