Binomial Products (1 of 2: Visualising the expansion)

More resources available at www.misterwootube.com

From playlist Further Algebraic Techniques

How can we represent any term in a binomial expansion

👉 Learn all about binomial expansion. A binomial expression is an algebraic expression with two terms. When a binomial expression is raised to a positive integer exponent, we usually use the binomial expansion technique to easily expand the power. The general formula for a binomial expans

From playlist Sequences

Properties of Binomial Coefficients (1 of 2: Symmetry & Row Totals)

More resources available at www.misterwootube.com

From playlist Working with Combinatorics

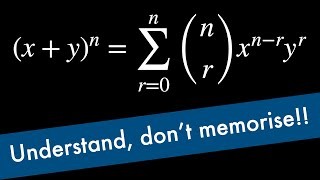

The Binomial Theorem | A-level Mathematics

Understanding the binomial theorem. Thanks for watching! This is applicable when the exponent of the binomial is a natural number. If the exponent is a fraction, you need a slightly different version of this theorem which is a topic for another video. ❤️ ❤️ ❤️ Support the channel ❤️

From playlist A-level Mathematics Revision

Pricing Options using Black Scholes Merton

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle The Black–Scholes or Black–Scho

From playlist Class 3: Pricing Financial Options

Pricing Options - Revision Lecture

These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter here: https://twitter.com/PatrickEBoyle

From playlist Revision Lectures

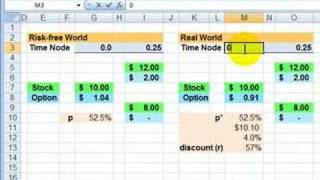

FRM: Risk neutral valuation in option pricing model

A difficult idea, but maybe the key idea in option pricing: we can price the option under the riskless assumption and yet it will be valid it the real (risky) world! For more financial risk videos, visit our website! http://www.bionicturtle.com

From playlist Derivatives: Option Pricing

Risk-neutral probabilities (FRM T5-07)

One of the harder ideas in fixed income is risk-neutral probabilities. In this video, I'd like to specifically illustrate, and define, what we mean by risk-neutral probabilities. I will do this in three steps. The first one is just a simple example of a coin toss, where my objective is to

From playlist Market Risk (FRM Topic 5)

Use binomial expansion to determine the 3rd term

👉 Learn how to find the given term of a binomial expansion. A binomial expression is an algebraic expression with two terms. When a binomial expression is raised to a positive integer exponent, we usually use the binomial expansion technique to easily expand the power. The general formula

From playlist Sequences

Greatest Binomial Coefficient (1 of 5: Review of prior theory)

More resources available at www.misterwootube.com

From playlist Working with Combinatorics

👉 Learn all about binomial expansion. A binomial expression is an algebraic expression with two terms. When a binomial expression is raised to a positive integer exponent, we usually use the binomial expansion technique to easily expand the power. The general formula for a binomial expans

From playlist Sequences

How to Price Options using a Binomial Tree (The Portfolio Approach)

How to Price Options using a Binomial Tree. The portfolio approach. These classes are all based on the book Trading and Pricing Financial Derivatives, available on Amazon at this link. https://amzn.to/2WIoAL0 Check out our website http://www.onfinance.org/ Follow Patrick on twitter her

From playlist Class 3: Pricing Financial Options

We look at some more advanced induction techniques, including strong induction. Please Subscribe: https://www.youtube.com/michaelpennmath?sub_confirmation=1 Merch: https://teespring.com/stores/michael-penn-math Personal Website: http://www.michael-penn.net Randolph College Math: http://w

From playlist Proof Writing

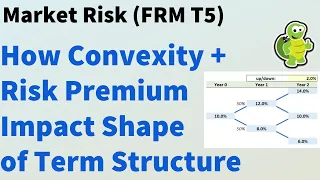

Convexity and risk premium impacts on shape of term structure (FRM T5-08)

In this video, I'm going to try to illustrate all of the important ideas that are in Tuckman's Chapter 8: The Evolution of Short Rates and the Shape of the Term Structure. This chapter discusses the shape of the term structure and the key influences on the shape of the spot rate term struc

From playlist Market Risk (FRM Topic 5)

What is a Binomial Tree? |Financial Risk Manager Training and Certification | Simplilearn

🔥Explore Our Free Courses With Completion Certificate by SkillUp: https://www.simplilearn.com/skillup-free-online-courses?utm_campaign=WhatIsABinomialTree&utm_medium=DescriptionFirstFold&utm_source=youtube This video explains the: 1.Binomial Models 2.One Step 3.Two Step 4.Modified and Amer

From playlist FRM Tutorial | Financial Risk Management Tutorial | Simplilearn

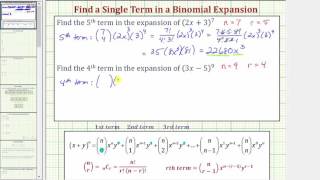

Ex: Find a Single Term in a Binomial Expansion

This video explains how to determine a single term in a binomial expansion. http://mathispower4u.com

From playlist Using the Binomial Theorem / Combinations

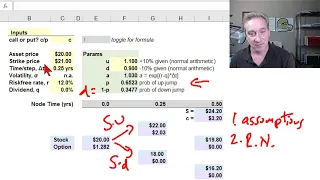

Introduction to binomial option pricing model: two-step (FRM T4-6)

[my xls is here https://trtl.bz/2AruFiH] The binomial option pricing model needs: 1. A set of assumptions similar but not identical to those found in Black-Scholes; 2. A framework; i.e., risk-neutral valuation which allows us to infer the probability of an up-jump; 3. An assumption about a

From playlist Valuation and RIsk Models (FRM Topic 4)

From playlist Binomial Theorem

Binomial tree option price: American-style (FRM T4-8)

[My xls is here https://trtl.bz/2DcTVeo ] An American-style option allows for early exercise; therefore, it must be worth more than the equivalent European option. To price the option with the binomial, we only need to modify the non-terminal nodes so that their value equals Max (expected

From playlist Valuation and RIsk Models (FRM Topic 4)