Basic stochastic simulation b: Stochastic simulation algorithm

(C) 2012-2013 David Liao (lookatphysics.com) CC-BY-SA Specify system Determine duration until next event Exponentially distributed waiting times Determine what kind of reaction next event will be For more information, please search the internet for "stochastic simulation algorithm" or "kin

From playlist Probability, statistics, and stochastic processes

Discrete-Time Dynamical Systems

This video shows how discrete-time dynamical systems may be induced from continuous-time systems. https://www.eigensteve.com/

From playlist Data-Driven Dynamical Systems

From playlist Contributed talks One World Symposium 2020

Jana Cslovjecsek: Efficient algorithms for multistage stochastic integer programming using proximity

We consider the problem of solving integer programs of the form min {c^T x : Ax = b; x geq 0}, where A is a multistage stochastic matrix. We give an algorithm that solves this problem in fixed-parameter time f(d; ||A||_infty) n log^O(2d) n, where f is a computable function, d is the treed

From playlist Workshop: Parametrized complexity and discrete optimization

Closed loop discrete controller Lecture 2019-04-08

Evaluating the response of a continuous system controlled by a discrete controller using several methods

From playlist Discrete

MIT RES.6-012 Introduction to Probability, Spring 2018 View the complete course: https://ocw.mit.edu/RES-6-012S18 Instructor: John Tsitsiklis License: Creative Commons BY-NC-SA More information at https://ocw.mit.edu/terms More courses at https://ocw.mit.edu

From playlist MIT RES.6-012 Introduction to Probability, Spring 2018

Random Processes and Stationarity

http://AllSignalProcessing.com for more great signal-processing content: ad-free videos, concept/screenshot files, quizzes, MATLAB and data files. Introduction to describing random processes using first and second moments (mean and autocorrelation/autocovariance). Definition of a stationa

From playlist Random Signal Characterization

(ML 19.2) Existence of Gaussian processes

Statement of the theorem on existence of Gaussian processes, and an explanation of what it is saying.

From playlist Machine Learning

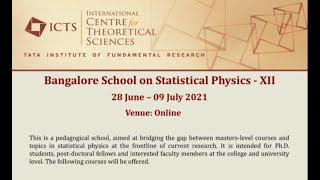

Markov processes and applications-3 by Hugo Touchette

PROGRAM : BANGALORE SCHOOL ON STATISTICAL PHYSICS - XII (ONLINE) ORGANIZERS : Abhishek Dhar (ICTS-TIFR, Bengaluru) and Sanjib Sabhapandit (RRI, Bengaluru) DATE : 28 June 2021 to 09 July 2021 VENUE : Online Due to the ongoing COVID-19 pandemic, the school will be conducted through online

From playlist Bangalore School on Statistical Physics - XII (ONLINE) 2021

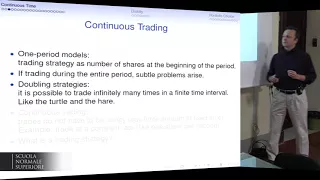

Paolo Guasoni, Lesson I - 18 december 2017

QUANTITATIVE FINANCE SEMINARS @ SNS PROF. PAOLO GUASONI TOPICS IN PORTFOLIO CHOICE

From playlist Quantitative Finance Seminar @ SNS

Stilian Stoev: Function valued random fields: tangents, intrinsic stationarity, self-similarity

We study random fields taking values in a separable Hilbert space H. First, we focus on their local structure and establish a counterpart to Falconer's characterization of tangent fields. That is, we show (under general conditions) that the tangent fields to a H-valued process are self-sim

From playlist Probability and Statistics

Introduction to Linear Time Invariant System Descriptions

http://AllSignalProcessing.com for free e-book on frequency relationships and more great signal processing content, including concept/screenshot files, quizzes, MATLAB and data files. Introduces systems and their use in signal processing; defines linearity, time invariance, and causal sys

From playlist Introduction and Background

2 Ruediger - Stochastic Integration & SDEs

PROGRAM NAME :WINTER SCHOOL ON STOCHASTIC ANALYSIS AND CONTROL OF FLUID FLOW DATES Monday 03 Dec, 2012 - Thursday 20 Dec, 2012 VENUE School of Mathematics, Indian Institute of Science Education and Research, Thiruvananthapuram Stochastic analysis and control of fluid flow problems have

From playlist Winter School on Stochastic Analysis and Control of Fluid Flow

Martin Schweizer: Some stochastic Fubini theorems

Find this video and other talks given by worldwide mathematicians on CIRM's Audiovisual Mathematics Library: http://library.cirm-math.fr. And discover all its functionalities: - Chapter markers and keywords to watch the parts of your choice in the video - Videos enriched with abstracts, b

From playlist Analysis and its Applications

Integrating Inference with Stochastic Process Algebra Models - Jane Hillston, Edinburgh

ProPPA is a probabilistic programming language for continuous-time dynamical systems, developed as an extension of the stochastic process algebra Bio-PEPA. It offers a high-level syntax for describing systems of interacting components with stochastic behaviours where some of the parameters

From playlist Logic and learning workshop

FinMath L2-2: The general Ito integral 2

Welcome to the second part of lesson 2. In this video we discuss some properties of the (general) Ito integral and introduce the necessary notions to deal with the Ito-Doeblin formula, which will be treated in Lesson 3. Topics: 00:00 A little exercise for you 06:46 Definition of the integ

From playlist Financial Mathematics

Markov processes and applications by Hugo Touchette

PROGRAM : BANGALORE SCHOOL ON STATISTICAL PHYSICS - XII (ONLINE) ORGANIZERS : Abhishek Dhar (ICTS-TIFR, Bengaluru) and Sanjib Sabhapandit (RRI, Bengaluru) DATE : 28 June 2021 to 09 July 2021 VENUE : Online Due to the ongoing COVID-19 pandemic, the school will be conducted through online

From playlist Bangalore School on Statistical Physics - XII (ONLINE) 2021

Sebastian Ertel - An Ensemble Kalman-Bucy filter for correlated observation noise

Sebastian Ertel (Technical University of Berlin) presents, "An Ensemble Kalman-Bucy filter for correlated observation noise", 8/7/22.

From playlist Statistics Across Campuses

Some solvable Stochastic Control Problems

At the 2013 SIAM Annual Meeting, Tyrone Duncan of the University of Kansas described stochastic control problems for continuous time systems where optimal controls and optimal costs can be explicitly determined by a direct method. The applicability of this method is demonstrated by example

From playlist Complete lectures and talks: slides and audio

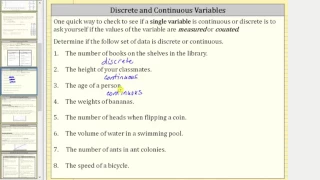

Introduction to Discrete and Continuous Variables

This video defines and provides examples of discrete and continuous variables.

From playlist Introduction to Functions: Function Basics